Subscribe and receive email notifications of new blog posts.

RSS Feed

RSS Feed

8

March 2026 Alabama Gulf Coast Real Estate Stats

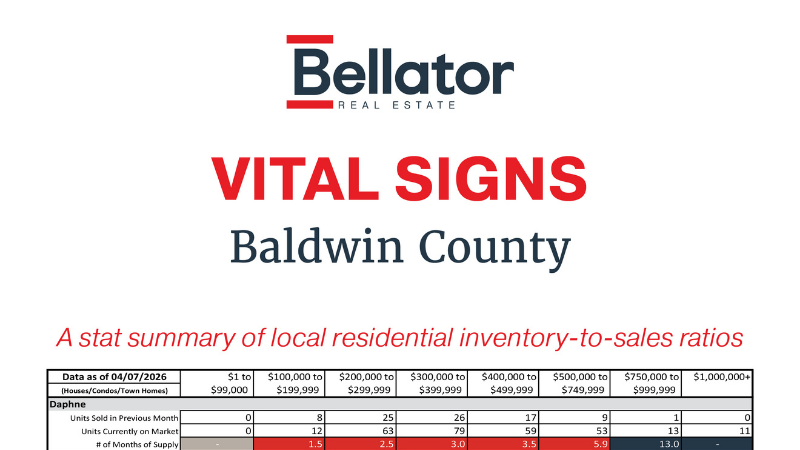

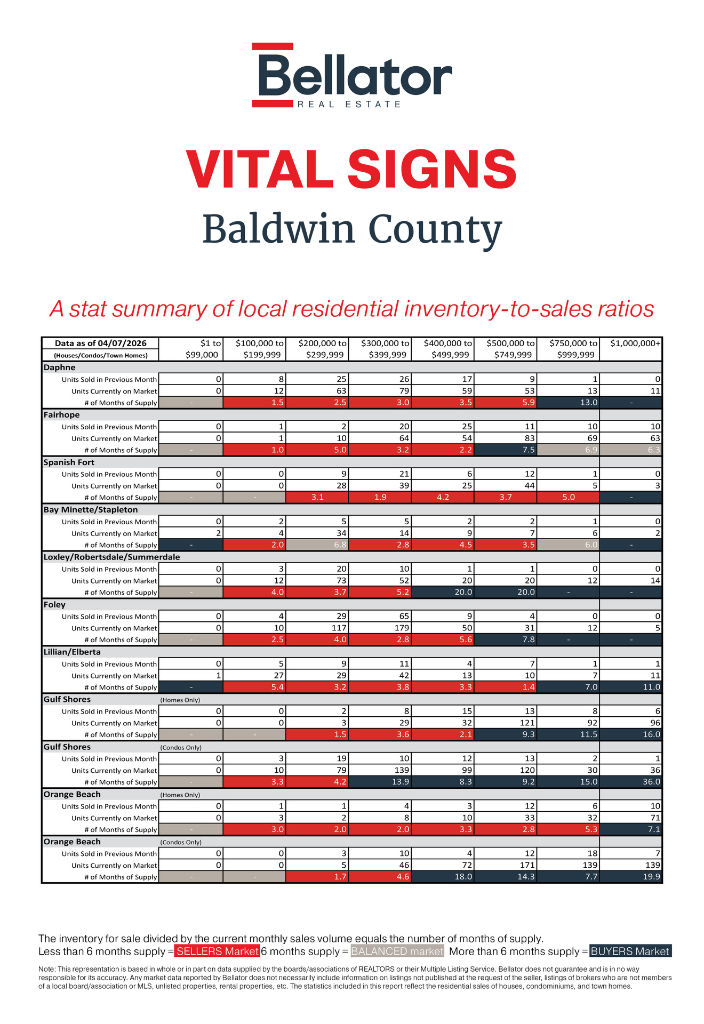

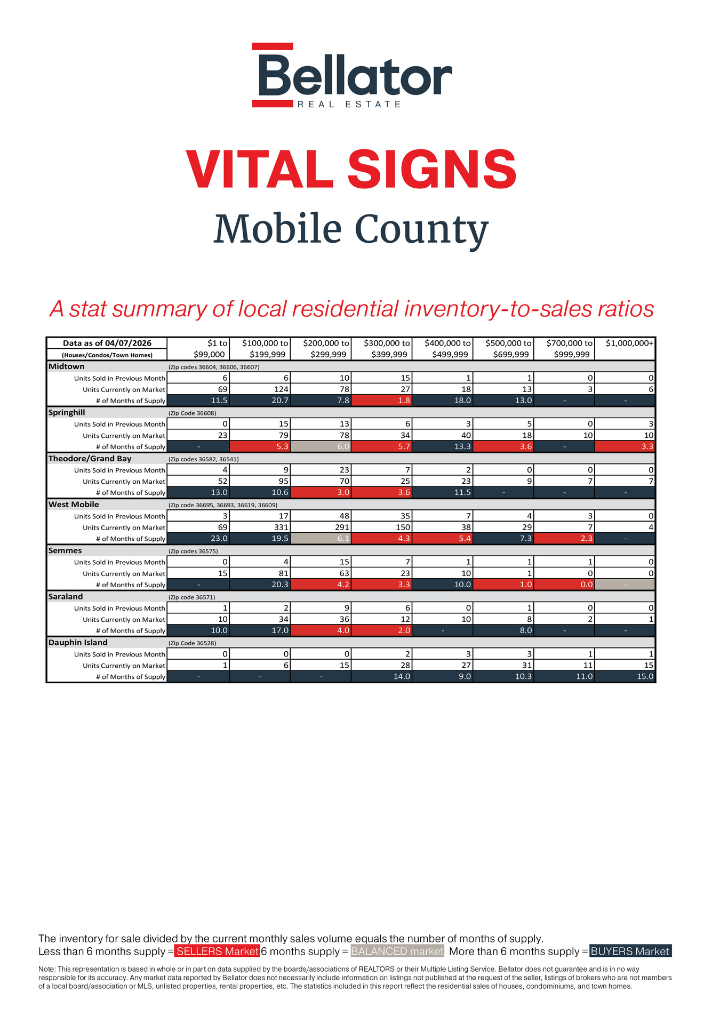

Vital Signs provides a visual representation of what's happening in the Alabama Gulf Coast real estate market. The color-coded numbers represent the absorption rate; the number of months it would take to sell every home on the market in a particular price range if no others were added. If the market is moving quickly, the absorption rate will fall below six months of supply, and if it's more of a buyer's market, it will jump above six months of supply. The rate is determined by dividing the number of units currently on the market by the number sold in the past month.

Baldwin County Real Estate Market Update

February to March 2026: The Spring Surge Arrives

If February felt like the market was stretching before a run, March was the full sprint. Across Baldwin County, we're seeing a clear seasonal shift: more sales, tightening inventory in key price ranges, and momentum building as we head into peak buying season.

Let's break it down.

Big Picture: What Changed?

March brought a noticeable jump in activity:

- Sales increased across most markets, especially in the $200K–$400K range

- Months of supply tightened, signaling stronger demand

- Inventory rose slightly in some areas, but was often absorbed quickly

- The market is trending toward balanced or even seller-leaning in many segments

In short: buyers are back, and they didn't come quietly.

Area-by-Area Breakdown

Daphne: From Steady to Strong

Daphne saw one of the most noticeable jumps in activity.

- Sales in the $200K–$400K range surged significantly

- Months of supply tightened across nearly all price points

- The $100K–$199K range dropped to just 1.5 months of supply

Takeaway: Daphne is heating up fast, with strong buyer demand creating a more competitive environment.

Fairhope: Luxury Strength + Mid-Range Stability

Fairhope continues to flex its muscles across multiple price points.

- Strong gains in $300K–$500K sales activity

- Inventory remained relatively stable, but absorption improved

- Months of supply dropped in several key segments

Takeaway: A healthy, balanced market with growing seller leverage, especially in desirable mid-to-upper price ranges.

Spanish Fort: A Sharp Rebound

Spanish Fort made a strong comeback in March.

- Sales jumped in the $300K–$500K range

- Months of supply dropped significantly, especially in:

- $300K–$400K (down to ~1.9 months)

- $500K–$750K (down to ~3.7 months)

Takeaway: This market shifted quickly toward sellers, particularly in move-up price points.

Bay Minette / Stapleton: Stabilizing After Volatility

- More consistent sales across price ranges

- Inventory fluctuated but remained manageable

- Months of supply normalized in most segments

Takeaway: A steadier, more predictable market after February's uneven activity.

Loxley / Robertsdale / Summerdale: Mixed Signals

- Sales improved slightly, especially under $300K

- Higher price points still show elevated supply (up to 20 months)

Takeaway: Entry-level homes are moving, but upper price ranges remain slower.

Foley: A Breakout Month

Foley had a standout March.

- Massive jump in $300K–$400K sales (65 units!)

- Months of supply dropped sharply in core price ranges

- Inventory increased slightly but was absorbed quickly

Takeaway: Foley is one of the hottest markets right now, especially for mid-range buyers.

Lillian / Elberta: Quietly Strengthening

- Sales increased across multiple price points

- Months of supply dropped significantly, especially:

- $500K–$750K (down to ~1.4 months)

Takeaway: A tightening market with growing demand and limited inventory in select ranges.

Coastal Markets: A Tale of Two Speeds

Gulf Shores

Homes:

- Increased activity in the $300K–$500K range

- Still higher inventory in luxury tiers

Condos:

- Big jump in $200K–$300K sales

- Months of supply dropped dramatically in several ranges

Takeaway: Condos are gaining traction, while higher-end homes still move at a slower pace.

Orange Beach

Homes:

- Strong increase in sales, especially $500K+

- Months of supply dropped significantly across the board

Condos:

- Increased sales, particularly in higher price points

- Inventory remains elevated but is improving

Takeaway: Momentum is building, especially in the luxury and second-home segments.

Key Trends to Watch

- The $200K–$400K Sweet Spot

This price range is the engine of the market:

- Highest sales volume

- Fastest inventory absorption

- Increasing competition

- Luxury Market Still Finding Its Rhythm

- Higher price points ($750K+) still show elevated months of supply

- But March brought improved activity, especially in coastal areas

- Spring Market Has Officially Arrived

- February was the warm-up

- March is the launchpad

- Expect continued momentum into April and May

Final Thoughts – Baldwin County

March painted a clear picture: Baldwin County is accelerating into a competitive spring market.

- Buyers are more active

- Sellers are gaining leverage in key segments

- Inventory is being absorbed faster than it's coming online in many areas

If February was a flicker, March is a steady flame.

Mobile County Real Estate Market Update

February to March 2026: Momentum Builds… Selectively

If Baldwin County was a roaring bonfire in March, Mobile County feels more like a series of controlled burns. Some areas ignited with strong buyer activity, while others are still smoldering under heavier inventory.

The headline?

Sales improved across many segments, but supply is still calling the shots in several markets.

Let's dig in.

Big Picture: What Changed?

March delivered a mix of progress and imbalance:

- Sales increased in several key price ranges, especially $200K–$400K

- Months of supply tightened in select areas, signaling improved demand

- However, many segments still show elevated inventory (6+ months)

- The market remains hyper-localized depending on price and location

Think of it as a patchwork quilt. Some squares are hot; others still cool to the touch.

Area-by-Area Breakdown

Midtown: A Tale of Two Markets

Midtown showed one of the most dramatic internal shifts.

- Sales in $300K–$400K jumped sharply (2 → 15 sales)

- Months of supply in that range dropped to just 1.8 months

- Meanwhile, lower price points ($100K–$200K) saw supply spike to 20.7 months

Takeaway:

Midtown is red-hot in the mid-range, but entry-level inventory is stacking up.

Springhill: Demand Awakens

Springhill came alive in March.

- Big jump in $100K–$200K sales (5 → 15)

- Improved absorption across most price ranges

- Months of supply dropped notably in:

- $100K–$200K (down to 5.3)

- $500K–$700K (down to 3.6)

Takeaway:

A clear shift toward balanced conditions, with buyers stepping back in.

Theodore / Grand Bay: Strong Mid-Range Activity

- Significant increase in $200K–$300K sales (12 → 23)

- Months of supply tightened to ~3.0 in that range

- Higher price points still show slower movement

Takeaway:

This market is gaining traction, especially for affordable and mid-range buyers.

West Mobile: Consistent but Competitive

West Mobile continues to be one of the most active areas.

- Strong sales growth in:

- $200K–$300K (42 → 48)

- $300K–$400K (29 → 35)

- Months of supply remained relatively stable in core price points (4–6 months)

- Some pressure building in higher price ranges

Takeaway:

A steady, balanced market with consistent buyer demand.

Semmes: Quiet Improvements

- Slight decline in sales volume in some ranges

- Months of supply improved in the $200K–$300K range (up to 4.2)

- Still elevated supply in lower price points

Takeaway:

Gradual stabilization, but still leaning toward a buyer's market overall.

Saraland: Small Market, Big Swings

- Sales increased in mid-range price points

- Months of supply dropped significantly in:

- $200K–$300K (down to 4.0)

- $300K–$400K (down to 2.0)

Takeaway:

A tightening market where limited inventory can shift conditions quickly.

Dauphin Island: Luxury Lag, Some Movement

- Modest increase in sales across mid-to-upper ranges

- Inventory remains high, especially:

- $500K+ segments (double-digit months of supply)

Takeaway:

A buyer's market persists, particularly in higher price points and vacation inventory.

Key Trends to Watch

- The $200K–$400K Engine

Just like Baldwin County, this range is doing the heavy lifting:

- Strongest sales growth

- Most consistent absorption

- Closest to balanced conditions

- Entry-Level Inventory Is Piling Up

- Many areas show 10+ months of supply under $200K

- Slower buyer activity in these price points

This could signal:

- Financing challenges

- Property condition issues

- Or shifting buyer preferences upward

- Upper-End Market Still Sluggish ?

- $500K+ price points remain inconsistent

- Some pockets improving, but many still over-supplied

Final Thoughts – Mobile County

March brought meaningful improvement, but Mobile County isn't moving in unison.

- Some areas are tightening fast

- Others are still working through excess inventory

- The market is becoming increasingly price-sensitive and location-driven

If February was a slow drumbeat, March added rhythm… just not a full orchestra yet.

Contact your Bellator agent today to strategize your next move to the Gulf Coast.

Privacy Policy / DMCA Notice / ADA Accessibility